Default, Not Thrift, Pares U.S. Debt

…

That sounds like a lot, but it’s better than it was before: At its peak in the first quarter of 2008, the debt-to-income ratio stood at 131%. Economists tend to see 100% as a reasonable level, so we’re almost a third of the way there.

…

Since household debt hit its peak in early 2008, banks have charged off a total of about $210 billion in mortgage and consumer loans, including credit cards. If one assumes that investors suffered at least that much in losses on similar loans that banks packaged and sold as securities (a very conservative assumption), then the total – that is, the amount of debt consumers shed through defaults – comes to much more than $400 billion.

Problem is, that’s more than the concurrent decrease in household debts, which amounts to only $372 billion, according to the Federal Reserve. That means consumers, on average, aren’t paying down their debts at all. Rather, the defaulters account for the whole decline, while the rest have actually been building up more debt straight through the worst financial crisis and recession in decades.

Interesting data, and not good news. We need to reduce consumer debt levels by reducing the borrowing we are doing. This is not a new need. We have been living beyond our means for far too long. That is not a solid base for an economy. It does boost current GDP but only by consuming future productive capacity (when you borrow from external sources – other countries – as we have been doing).

Related: USA Consumer Debt Stands at $2.44 Trillion – How a Family Shed $106,000 in Debt

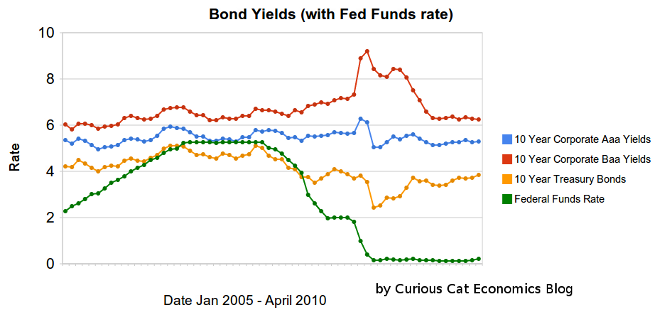

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,