USA health care spending continues to grow, consuming an ever increasing share of the economic production of the USA. USA health care spending is twice that of other rich countries for worse health care results.

- USA health care expenditures grew 3.9% to $2.7 trillion in 2011, or $8,680 per person, and accounted for 17.9% of Gross Domestic Product (GDP).

- Medicare spending grew 6.2% to $554.3 billion in 2011, to 21% of total health care spending.

- Medicaid spending grew 2.5% to $407.7 billion in 2011, or 15% of total health care spending.

- Private health insurance spending grew 3.8% to $896.3 billion in 2011, or 33 percent of total health care expenditures.

- Out of pocket spending grew 2.8% to $307.7 billion in 2011, or 11 percent of total health care spending.

- Hospital expenditures grew 4.3% to $850.6 billion in 2011.

- Physician and clinical services expenditures grew 4.3% to $541.4 billion in 2011.

- Prescription drug spending increased 2.9% to $263.0 billion in 2011.

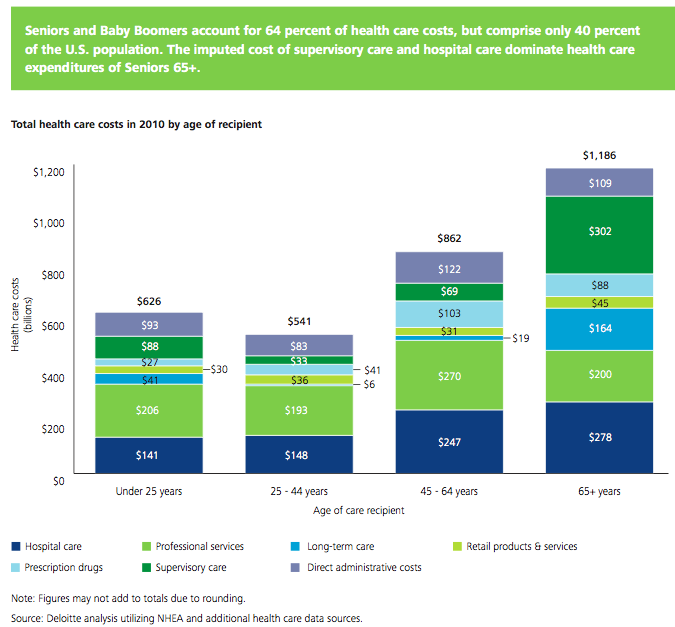

- Per person personal health care spending for the 65 and older population was $14,797 in 2004, 5.6 times higher than spending per child ($2,650) and 3.3 times spending per working-age person ($4,511).

Individuals (28%) and the federal government (28%) accounted for the largest share of those paying for health care in the USA. Businesses pay 21% of the costs of health care while state and local governments pay 17%.

The United States Centers for Medicare & Medicaid Services (CMS) project that health care spending will rise to 19.6% of GDP by 2021. Since the long term failure of the USA health care system has resulted in costs increasing faster than inflation every year for decades, it seems reasonable to expect that trend to continue. The burden on the USA grows more and more harmful to the USA each year these rising costs continue.

In 2004, the elderly (65 years old and older) accounted for 12% of the population, and accounted for 34% of spending.

Data from US CMS (sadly the way they provide the data online my guess is this url will fail to work in a year, as they post the updated data – I don’t see a way to provide a link to a url with persistent data).

Half of the population spends little or nothing on health care, while 5% of the population spends almost half of the total amount (The High Concentration of U.S. Health Care Expenditures: Research in Action).

Related: USA Spends Record $2.5 Trillion, $8,086 per person 17.6% of GDP on Health Care in 2009 – USA Spent $2.2 Trillion, 16.2% of GDP, on Health Care in 2007 – USA Health Care Costs reach 15.3% of GDP – the highest percentage ever (2005) – Systemic Health Care Failure: Small Business Coverage