William Black wrote The Best Way to Rob a Bank Is to Own One: How Corporate Executives and Politicians Looted the S&L. I think he a bit off on the “owning one,” being the best way to loot. The looters are not owners, they are executives that loot from owners, taxpayers, customers… And those looters pay politicians a great deal of money to help them. He appeared on Bill Moneys Journal discussing the huge mess we know are in and how little is being done to hold those responsible for the enormous crisis created by them.

Fraud is deceit. And the essence of fraud is, “I create trust in you, and then I betray that trust, and get you to give me something of value.” And as a result, there’s no more effective acid against trust than fraud, especially fraud by top elites, and that’s what we have.

…

The FBI publicly warned, in September 2004 that there was an epidemic of mortgage fraud, that if it was allowed to continue it would produce a crisis at least as large as the Savings and Loan debacle. And that they were going to make sure that they didn’t let that happen. So what goes wrong? After 9/11, the attacks, the Justice Department transfers 500 white-collar specialists in the FBI to national terrorism. Well, we can all understand that. But then, the Bush administration refused to replace the missing 500 agents. So even today, again, as you say, this crisis is 1000 times worse, perhaps, certainly 100 times worse, than the Savings and Loan crisis. There are one-fifth as many FBI agents as worked the Savings and Loan crisis.

…

Well, certainly in the financial sphere, I am. I think, first, the policies are substantively bad. Second, I think they completely lack integrity. Third, they violate the rule of law. This is being done just like Secretary Paulson did it. In violation of the law. We adopted a law after the Savings and Loan crisis, called the Prompt Corrective Action Law. And it requires them to close these institutions. And they’re refusing to obey the law.

…

In the Savings and Loan debacle, we developed excellent ways for dealing with the frauds, and for dealing with the failed institutions. And for 15 years after the Savings and Loan crisis, didn’t matter which party was in power, the U.S. Treasury Secretary would fly over to Tokyo and tell the Japanese, “You ought to do things the way we did in the Savings and Loan crisis, because it worked really well. Instead you’re covering up the bank losses, because you know, you say you need confidence. And so, we have to lie to the people to create confidence. And it doesn’t work. You will cause your recession to continue and continue.”

…

And their ideologies, which swept away regulation. So, in the example, regulation means that cheaters don’t prosper. So, instead of being bad for capitalism, it’s what saves capitalism. “Honest purveyors prosper” is what we want. And you need regulation and law enforcement to be able to do this. The tragedy of this crisis is it didn’t need to happen at all.

Related: Fed Continues Wall Street Welfare – Credit Crisis the Result of Planned Looting of the World Economy – Lobbyists Keep Tax Off Billion Dollar Private Equities Deals – Poll: 60% say Depression Likely – Canadian Banks Avoid Failures Common Elsewhere – Too Big to Fail – Why Pay Taxes or be Honest

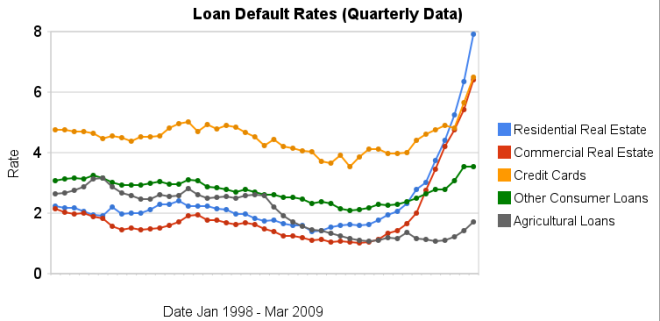

Chart showing loan default rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog, Creative Commons Attribution, data from the Federal Reserve.

Chart showing loan default rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog, Creative Commons Attribution, data from the Federal Reserve. Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From