I do not like the actions of many in “private equity.” I am a big fan of capitalism. I also object to those that unjustly take from the other stakeholders involved in an enterprise. It is not the specific facts of this case, that I see as important, but the thinking behind these types of actions. Which specific actions are to blame for this bankruptcy is not my point. I detest that financial gimmicks by “private capital” that ruin companies.

Those gimmicks that leave stakeholders that built such companies in ruin should be criticized. It is a core principle that I share with Dr. Deming, Toyota… that companies exist not to be plundered by those in positions of power but to benefit all the stakeholders (employees, owners, customers, suppliers, communities…). I don’t believe you can practice real lean manufacturing and subscribe to this take out cash and leave a venerable company behind kind of thinking.

How Private Equity Strangled Mervyns

When those firms bought Mervyns from Target for $1.2 billion in 2004, they promised to revive the limping West Coast retailer. Then they stripped it of real estate assets, nearly doubled its rent, and saddled it with $800 million in debt while sucking out more than $400 million in cash for themselves, according to the company. The moves left Mervyns so weak it couldn’t survive.

Mervyns’ collapse reveals dangerous flaws in the private equity playbook. It shows how investors with risky business plans, unrealistic financial assumptions, and competing agendas can deliver a death blow to companies that otherwise could have survived. And it offers a glimpse into the human suffering wrought by owners looking to turn a quick profit above all else.

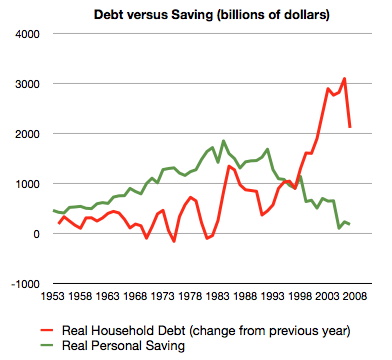

Too much debt is not just a personal finance problem it is a problem for companies too. Continue reading on my original post on the Curious Cat Management Blog.

Related: Leverage, Complex Deals and Mania – Failed Executives Used Too Much Leverage – posts on debt