In my opinion is has never been more difficult to plan for retirement. It is extremely difficult to guess what rates of return should be expected in the next 10-30 years. It might have actually been as difficult 10 years ago, but it seemed that it wasn’t. Estimating a 7-8% return for your portfolio seemed a pretty reasonable thing to do, and evening considering 10% wasn’t unthinkable, if you wanted to be optimistic and took more risk.

Today it is very hard to guess, going forward, what is reasonable. It is also hard to find any very safe decent yields. Is 4% a good estimate for your portfolio? 6%? 8%? What about inflation? I know inflation isn’t a huge concern of people right now, but I still think it is a very real risk. I think trying to project is helpful (even with all the uncertainty). But it is more important than ever to look at various scenarios and consider the risks if things don’t go as well as you hope. The best way to deal with that is to save more.

In the USA save at least 10% of your income for retirement in your own savings (in addition to social security) and it would be better to save 12% and you might even need to be saving 15%. And if you waited beyond 30 to start doing this you have to save substantially more, to have a comfortable retirement plan (obviously if you are willing to live at a much lower standard of living in retirement than before, you can save less).

Other factors matter too. If you don’t own your house with no more mortgage payments you will need to save more. Ideally you will have not debts at retirement, if you do, again you need to save more.

That Retirement Calculator May Be Lying to You

According to Ibbotson data, the long-term annualized gain for the Standard & Poor’s 500-stock index dating back to 1926 is 9.9 percent. For bonds, it’s 5.4 percent. (From 1970 to 2010, the Barclays Capital Aggregate Bond index average was 8.3 percent.) Plug those numbers into a portfolio of 60 percent stocks and 40 percent bonds and the return is about 8 percent, which is precisely the number most financial planners — and retirement calculators — were using up until recently.

…

Vanguard founder Jack Bogle has a slightly more upbeat assessment. He expects stock returns of 7 percent to 7.5 percent over the next decade. He assumes no expansion in the market’s price-earnings ratio, dividend yields of 2.2 percent, and earnings growth of at least 5 percent. Bogle expects bond returns to be about 3 percent. For a balanced portfolio, that produces a net nominal return of slightly more than 6 percent. A higher forecast is T. Rowe Price’s estimate of 7 percent; until this year it had used 8 percent.

I also suggest using high quality high yield dividend stocks for more of the bond portfolio. I wouldn’t hold bonds with maturities over 5 years at these yields (or if I did, they would be an extremely small portion of the portfolio). I would also have a fair amount of the bond portfolio in inflation protected bonds.

I also invest in emerging economies like China, Brazil, India, Malaysia, Indonesia, Thailand, the continent of Africa… To some extent you get that with large companies like Google, Intel, Tesco, Toyota, Apple… that are making lots of money in emerging economies and continuing to invest more in emerging markets. VWO (.22% expense ratio) is a good exchange traded fund (ETF) for emerging markets. I also believe investing in real estate is wise as part of a retirement portfolio.

Related: 401(k) Options, Select Low Expenses – How Much Will I Need to Save for Retirement? – Investment Risk Matters Most as Part of a Portfolio, Rather than in Isolation

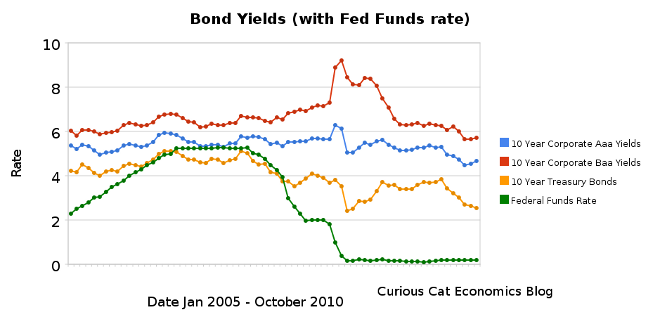

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,