See the full list of Dividend Aristocrats below. The stocks in this index are companies within the S&P 500 that have increased dividends every year for at least 25 consecutive years. After 10 were added and 1 removed, this month, there are now 51 companies included (so just over 10% of all S&P 500 stocks) – and remember many S&P 500 stocks haven’t existed for 25 years, or pay no dividend today, or didn’t 10 or 20 years ago (Google, Apple, Intel, …). It is surprising so many companies have successfully done this.

I’ll take a look at a few of them here (I looked at the new additions in my previous post: Investing in stocks that have raised dividends consistently).

| Stock | Yield |

|

div/share 2011 | div/share 2000 | % increase |

|---|---|---|---|---|---|

| 3M (MMM) | 2.8% | $2.20 | $1.16 | 90% | |

| Aflac (AFL) | 3.2% | $1.23 | $0.165 | 645% | |

| Abbott Laboratories (ABT) | 3.5% | $1.92 | $0.74 | 159% | |

| Cincinnati Financial (CINF) | 5.3% | $1.60 | $0.69 | 132% | |

| Coca-Cola Co (KO) | 2.8% | $1.88 | $0.68 | 176% | |

| Exxon Mobil Corp (XOM) | 2.4% | $1.85 | $0.88 | 110% | |

| Johnson & Johnson (JNJ) | 3.6% | $2.25 | $0.62 | 263% | |

| Kimberly-Clark (KMB) | 3.9% | $2.80 | $1.08 | 159% | |

| Medtronic (MDT) | 2.8% | $0.94 | $0.18 | 417% | |

| Procter & Gamble (PG) | 3.2% | $2.06 | $.67 | 207% |

Just looking at this data Aflac sure looks appealing. Having both a high yield and strong growth is an appealing combination. And Warren Buffet agree (he owns quite a bit) which is also reassuring (he also owns a large stake in Coke). Of course strong growth over the last 11 years won’t necessarily repeat (in fact it gets much harder). On the other had some slow growth companies would likely continue slow growth (at best): Exxon Mobil, 3M…

Really almost all of these stocks are pretty attractive. Medtronic, Johnson & Johnson and Abbot Laboratories look particularly appealing to me (along with Aflac and Kimberly-Clark). I would have to do more research on any of these (other than Abbot Laboratories, which I already own) before deciding to buy, but they sure look good as safe long term investments. Health care is a growing need (in the USA and globally). It is true the costs in the USA have to be reduced, and this could make things more difficult for companies in the health care industry.

Related: Sleep well investing portfolio – Looking for Dividend Stocks in the Current Extremely Low Interest Rate Environment – Is the Stock Market Efficient?

Full list of Dividend Aristocrats, an index measures the performance of large cap, blue chip companies within the S&P 500 that have followed a policy of increasing dividends every year for at least 25 consecutive years.

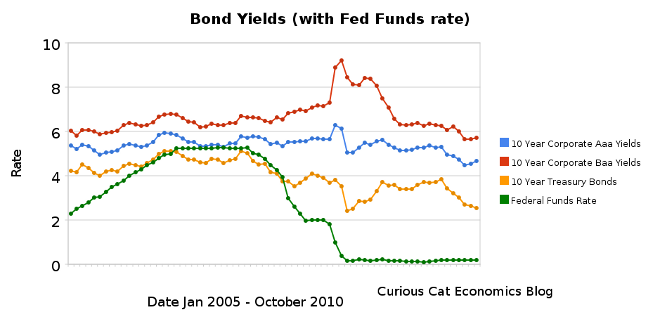

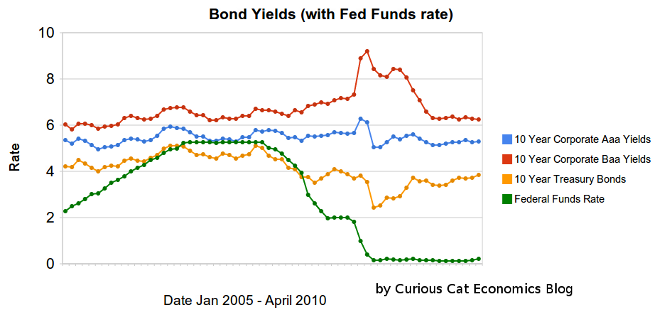

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,  Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,