Low Mortgage Rates a Mirage as Fees Climb, Eligibility Tightens

…

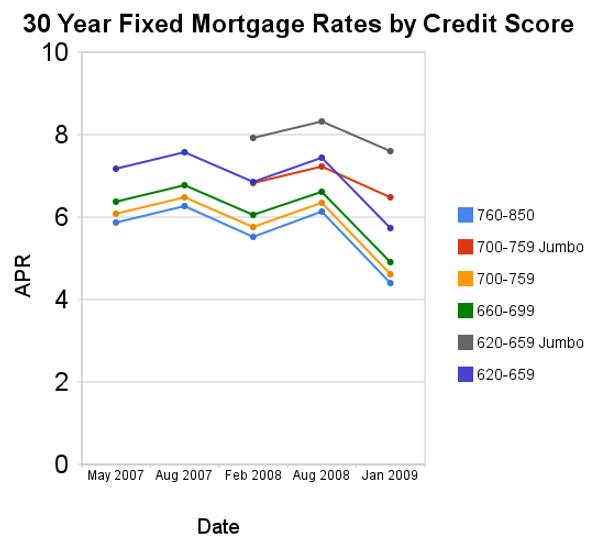

“A score of 700 was once near perfect,” said Gwen Muse Evans, vice president of credit policy at Fannie Mae, the government-controlled company that helps set lending standards. “Today, a 700 performs more like a 660 did. We have updated our policy to take into account the drift in credit scores.”

Consumer credit scores, called FICOs after creator Fair Isaac Corp., range from 300 to 850. The average FICO score on mortgages bought by Freddie Mac and Fannie Mae rose to 747.5 in the fourth quarter of last year from 722.3 in 2005, according to Inside Mortgage Finance.

Accunet’s Wickert said that a 660 FICO score would have qualified most borrowers for loans with no upfront fees in the past. Now, someone trying to borrow $200,000 with a 660 score would have to pay a 2.8 percent fee, or $5,600, he said. Even someone with a 719 score would have to pay $1,750 in cash.

The low mortgage rates are attractive but a decision to re-finance (or buy) must consider the long term implications. Also if you are re-financing to take advantage of the low rates consider a 20 year or 15 year loan if you are already well into your 30 year loan. A fixed rate loan is the most sensible option at this time.

Related: Low Mortgage Rates Not Available to Everyone – 30 Year Fixed Mortgage Rates and the Fed Funds Rate Chart – Ignorance of Many Mortgage Holders – Fed Plans To Curb Mortgage Excesses – How Not to Convert Home Equity