It’s Now a Renter’s Market by Prashant Gopal

Effective rents fell in 64 of 79 markets that Reis tracks. Effective rents in San Francisco dropped 2.8% in the first quarter of this year, compared with the previous quarter—the nation’s largest quarterly decline. Rents fell 2.6% in New York City (all five boroughs), 1.3% in Charlotte, 2.5% in San Jose, 0.9% in San Antonio, 0.9% in Cleveland, 1.2% in Chicago, and 2.3% on Long Island.

…

Oklahoma City, where people spent just 12% of their income on rent, was the most affordable. Other cheap markets included Indianapolis, Denver, Fort Worth, and Cleveland. The least affordable market was New York, where people spent 57% of their income on rent.

…

Oklahoma City, where people spent just 12% of their income on rent, was the most affordable. Other cheap markets included Indianapolis, Denver, Fort Worth, and Cleveland. The least affordable market was New York, where people spent 57% of their income on rent.

Rental markets are driven largely by 2 factors, vacancy rates and jobs. If jobs in a metropolitan area are increasing rents usually increase. If more new apartments are added to the market than jobs (which then increases vacancy rates) this will push down rates. Other factors influence vacancy rates (such as people moving back in with parent, people sharing apartments…). Those factors often are largely influenced by losing jobs in an area.

D.C. apartment market remains strong

The D.C. area continues to boast one of the best apartment markets in the U.S., with a vacancy rate well below the national number

…

Rent increases over the past 12 months for all investment grade apartments kept under the long-term average of 4.2 percent per annum, at 0.5 percent since March 2008.

…

Rent increases over the past 12 months for all investment grade apartments kept under the long-term average of 4.2 percent per annum, at 0.5 percent since March 2008.

Related: Housing Rents Falling in the USA – Home Values and Rental Rates – Real estate investing articles – Urban Planning – Longer Commutes Translate to Larger Housing Price Declines

(more…)

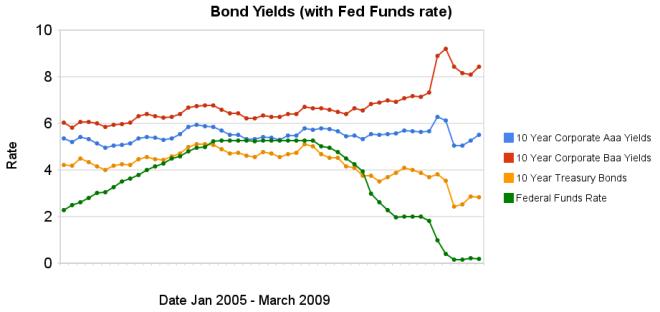

Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,