Landlords Offer Incentives to Stay Put

In the third quarter, the national apartment-vacancy rate hit 7.8%, a 23-year high, according to Reis Inc., which tracks vacancies and rents in the top 79 markets.

…

One problem for landlords is that existing tenants can easily check the Web to see what deals new tenants are being offered. And new tenants are getting incentives like a waived pet deposit or two months’ free rent.

…

Apartment landlords say that one benefit of the bad market is that it has practically halted new construction. New completions are expected to be 98,000 next year and 109,000 in 2011, compared with 188,000 last year and 204,000 this year, according to Green Street Advisors Inc.

…

One problem for landlords is that existing tenants can easily check the Web to see what deals new tenants are being offered. And new tenants are getting incentives like a waived pet deposit or two months’ free rent.

…

Apartment landlords say that one benefit of the bad market is that it has practically halted new construction. New completions are expected to be 98,000 next year and 109,000 in 2011, compared with 188,000 last year and 204,000 this year, according to Green Street Advisors Inc.

But when loss rates are taken into account—the removal of units because of obsolescence—the actual addition will be immaterial. That means that when the economy rebounds, the supply will be tight, increasing landlord profits.

Related: Apartment Vacancy at 22-Year High in USA (July 2009) – Articles on Real Estate Investing – It’s Now a Renter’s Market – Housing Rents Falling in the USA

Chart showing loan delinquency rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog,

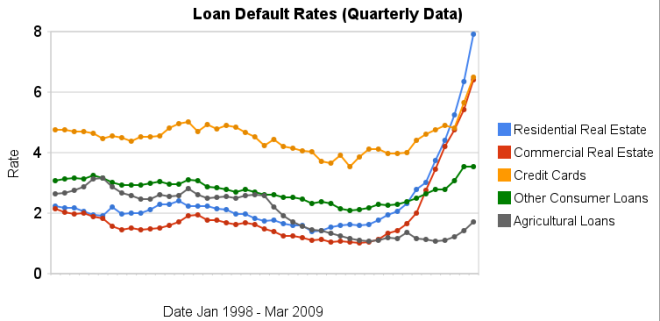

Chart showing loan delinquency rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog,  Chart showing loan default rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog,

Chart showing loan default rates for real estate, consumer and agricultural loans for 1998 to 2009 by the Curious Cat Investing Economics Blog,  Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 6 months. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate.

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From

Showing mortgage rates over the last 5 years. Red: 30 year fixed rate. Blue: 15 year fixed rate. Tan: 1 year adjustable rate. From