Welcome to the False Recovery by Eric Janszen

Companies planning for sudden and relatively near-term growth should reshape their strategies to make the best of economic flatness.

He makes a decent point for companies, but the he flips back and forth between the need to save more (because we are buried in debt) and the need to spend more (because we need to grow the economy right now). And while I wouldn’t stake my life on it I wouldn’t be surprised that we have a strong economic rebound (it is also perfectly conceivable we have a next to no growth or even fall into a recession). But it seems to me the return to bubble thinking and spending beyond our means is making a strong comeback.

Another ok, point but we have hardly paying off anything of the previous living beyond our means. It would take decades at this rate.

So the problem is the saving are not actually resulting in increased ability to spend (first point above) – which is bad he says, because it means their won’t be more spending (because people won’t have the ability to spend). Then he says when banks lend the consumers money they will spend and the saving rate will go down (which is bad – though he doesn’t seem to really want more savings (because that means business won’t get increased sales).

The conventional wisdom likes to point out the long term problem of low savings rate but then quickly point out we need more spending or the economy will slow. Yes, when you have an economy that is living beyond its means if you want to address the long term consequences of that it means you have to live within your means. It isn’t tricky. We need to save more. If that means the economy is slower compared to when we lived beyond our means that is what it takes. The alternative is just to live beyond your means for longer and dig yourself deeper into debt.

(more…)

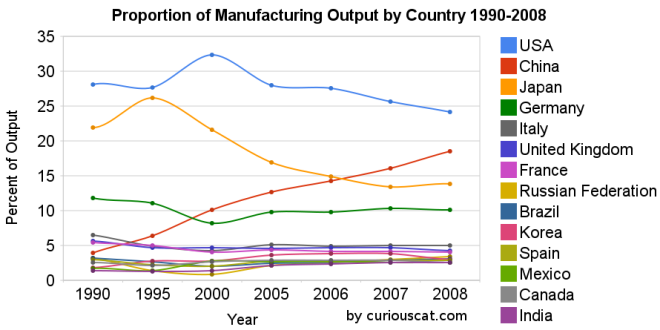

Chart showing the percentage output of top manufacturing countries from 1990-2008 by Curious Cat Management Blog,

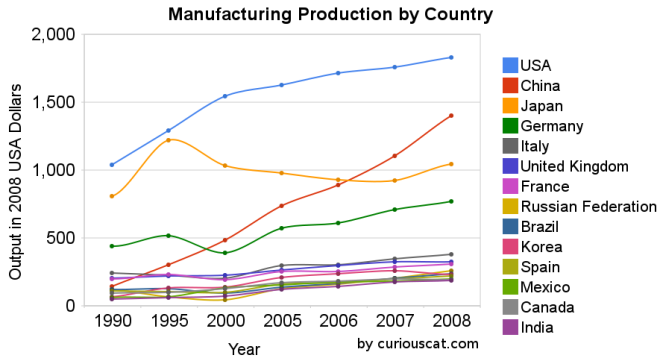

Chart showing the percentage output of top manufacturing countries from 1990-2008 by Curious Cat Management Blog,  Chart showing the output of the top manufacturing countries from 1990-2008 by Curious Cat Management Blog,

Chart showing the output of the top manufacturing countries from 1990-2008 by Curious Cat Management Blog,