Retiring overseas has been growing in popularity over the recent decades. A lower cost of living and health care systems that work are two of the big draws. Americans Who Seek Out Retirement Homes Overseas

…

She said a minimum amount for a comfortable retirement in a number of appealing places — Cuenca, Ecuador, and La Barra, Uruguay, being two examples — would be about $1,200 a month.

Mr. Holman said that if you purchased a home in Medellin, you could live quite comfortably on less than $2,000 a month. As time goes on, retirement hot spots change along with countries’ economic and political situations.

Ms. Peddicord said she used to recommend Ireland, Thailand and Costa Rica, but no longer does. She cited the high cost of living in Ireland, the anti-foreign sentiments in Thailand, and the growing crime rates both within and outside of San Jose, the Costa Rican capital.

…

“In Panama, for example, your rent could be $1,500 a month for a two-bedroom apartment in a nice building in Panama City with a doorman and a pool,” Ms. Peddicord said, “or it could be $200 a month if you choose instead to settle in a little house near the beach in Las Tablas, a beautiful, welcoming region.”

Lee Harrison, an American who retired to Ecuador several years ago and then moved in 2006 to Uruguay, said there were a wide range of financial issues to consider before making the leap to retire abroad.

For example, he recommends that retirees maintain a bank account and credit cards in their country of origin as well as in their new country, to facilitate money transfer. He also said that retirees should investigate their home country’s system of sending pension money to retirees abroad, as well as their new destination’s ability to accept electronic bank transfers.

Retirees also should request help from a tax adviser and make certain their move doesn’t trigger the need for a new will.

…

Financial considerations aside, advisers say that when making the decision to retire abroad, most retirees find that the journey itself is the reward.

“I know lots of people who retired to one country and then decided to move again somewhere else but never back” to their home, Ms. Peddicord said. “I don’t know of anyone who has decided to move back full-time after having had a taste of living abroad.”

Living overseas is something a significant portion of people in the USA have no interest in at all. But for those that like the idea there are appealing options with some strong benefits. At the same time you need to understand the significant change this bring to your life and plan for it I suggest visiting the location several times over the years – before you retire.

Related: In the USA 43% Have Less Than $10,000 in Retirement Savings – Many Retirees Face Prospect of Outliving Savings – Saving for Retirement

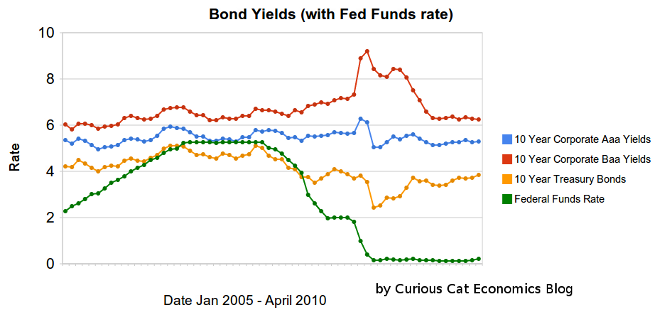

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,