Jumbo Loan Defaults Rise at Fast Pace as Rich Suffer

About 2.57 percent of prime borrowers who took out jumbo loans last year were at least 60 days delinquent

2.57% of homeowners with jumbo mortgage are 60 days late, of those that just got loan last year! That is crazy. These kinds of figures are astounding to me. I am still (posted Feb 2007) amazed that 4.4% is the historic low for mortgages over a month late.

About 1.92 percent of homeowners with 2008 mortgages backed by Fannie Mae and Freddie Mac fell at least 60 days behind, LPS Applied Analytics said. Jumbo loans are bigger than what the two government-controlled agencies buy or guarantee, and Obama’s plan focuses on shoring up mortgages eligible to be bought by Fannie and Freddie.

…

The top five U.S. jumbo lenders — Chase Home Finance LLC, Bank of America Corp., Washington Mutual Inc., Wells Fargo & Co. and Citigroup Inc. — originated a combined $55.3 billion in jumbos in 2008. They lent just $4.3 billion of that during the last three months of the year, according to Inside Mortgage Finance.

…

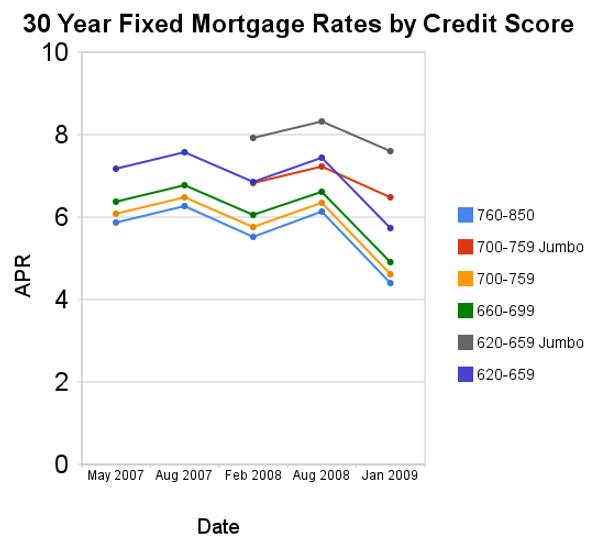

The national average for a 30-year fixed-rate jumbo mortgage was 6.57 percent this week compared with 5.34 percent for a conforming loan, according to White Plains, New York-based financial data provider BanxQuote.

…

The top five U.S. jumbo lenders — Chase Home Finance LLC, Bank of America Corp., Washington Mutual Inc., Wells Fargo & Co. and Citigroup Inc. — originated a combined $55.3 billion in jumbos in 2008. They lent just $4.3 billion of that during the last three months of the year, according to Inside Mortgage Finance.

…

The national average for a 30-year fixed-rate jumbo mortgage was 6.57 percent this week compared with 5.34 percent for a conforming loan, according to White Plains, New York-based financial data provider BanxQuote.

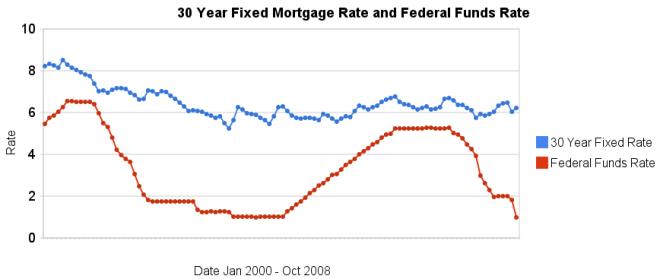

Related: The Impact of Credit Scores and Jumbo Size on Mortgage Rates – Low Mortgage Rates Not Available to Everyone – 30 Year Fixed Mortgage Rates and the Fed Funds Rate – posts about mortgages