Total nonfarm payroll employment grew by 431,000 in May but that total includes the hiring of 411,000 temporary employees to work on Census 2010, the U.S. Bureau of Labor Statistics reported today. Private-sector employment changed little (+41,000). Manufacturing, temporary help services, and mining added jobs, while construction employment declined. Economists were predicting over 500,000 job gains (given the large number of temporary census hires).

In order to substantially increase the job prospects going forward we need to average over 250,000 new jobs a month to make up for the lost jobs due to the credit crisis. The economy needs to gain about 125,000 jobs a month to keep up with population growth. The temporary census jobs help but those jobs are temporary so can’t be counted on for long term improvement in the job picture.

The number of unemployed persons was 15.0 million in May. The unemployment rate edged down to 9.7 percent, the same rate as in the first 3 months of 2010. The unemployment rates for adult men stand at 9.8%, 8.1% for adult women and 26.4% for teenagers.

In May, the number of long-term unemployed (those jobless for 27 weeks and over) was about unchanged at 6.8 million. These individuals made up 46.0 percent of unemployed persons, about the same as in April.

In May, the civilian labor force participation rate edged down by 20 basis points to 65%. The employment-population ratio was about unchanged over the month at 58.7%.

Among the marginally attached, there were 1.1 million discouraged workers in May, up by 291,000 from a year earlier. (The data are not seasonally adjusted.) Discouraged workers are persons not currently looking for work because they believe no jobs are available for them. The remaining 1.1 million persons marginally attached to the labor force had not searched for work in the 4 weeks preceding the survey for reasons such as school attendance or family responsibilities.

Manufacturing employment has risen by 126,000 over the past 5 months. Within manufacturing, both fabricated metals and machinery added jobs in May. Temporary help services added 31,000 jobs over the month; employment in the industry has risen by 362,000 since September 2009.

Government employment rose by 390,000 in May. The Federal government hired 411,000 temporary workers for Census 2010, bringing total temporary census staffing during the payroll survey reference period to 564,000. Employment in state government excluding education decreased by 13,000.

In May, the average workweek for all employees on private nonfarm payrolls increased by 0.1 hour to 34.2 hours. The manufacturing workweek for all employees increased by 0.3 hour to 40.5 hours. The average workweek for production and nonsupervisory employees on private non-

farm payrolls increased by 0.1 hour to 33.5 hours over the month.

Average hourly earnings of all employees in the private nonfarm sector increased by 7 cents, or 0.3 percent, to $22.57 in May. Over the past 12 months, average hourly earnings have increased by 1.9 percent. In May, average hourly earnings of private-sector production and nonsupervisory employees increased by 4 cents, or 0.2 percent, to $18.99.

The change in total nonfarm payroll employment for March was revised from +230,000 to +208,000, while the change for April remained at +290,000.

Related: USA Added 290,000 Jobs In April – Unemployment Rate Reached 10.2% (Nov 2009) – Another 663,000 Jobs Lost in March, 2009 in the USA

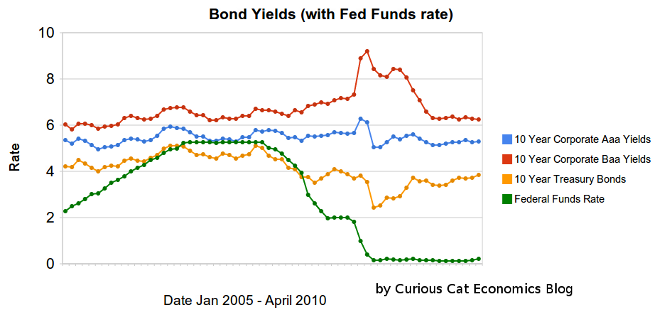

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,