Peet’s Coffee: In Africa, Brewing Good Works by Steve Hamm

…

Because of bad roads and delays at border crossings, it took 12 days for a truck with a container full of green coffee beans to travel 1,000 miles to the Kenyan port of Mombasa. The sea journey from Mombasa took nearly two months. Worse, when the shipment arrived in Oakland, Calif., in late February, a portion of the coffee was slightly damaged.

Moayyad traveled to Rwanda to cement relationships with farmer groups and gather stories about the farmers for use in marketing. With a videographer tagging along, she navigated molar-crunching roads in a four-wheel-drive pickup to remote villages and farms perched on hillsides high above Rwanda’s Lake Kivu. On the roadsides, children greeted the passing truck with an excited cry of “Abazungu [white people]!” Moayyad plans to post a journal of her travels on Peet’s Web site, aimed at the company’s most loyal customers, called Peetniks.

A good effort. Real world issues confront you when you take steps to build the capacity for capitalism to help people live better lives. We need more such efforts to help capitalists make better lives for themselves around the world.

Related: Bill Gates: Capitalism in the 21st Century – International Development Fair, The Human Factor – Helping Capitalism Create a Better World – Frontline Explores Kiva in Uganda

photo of Cesar Augusto SantamarÃa Escoto in his welding workshop, Chinandega, Nicaragua.

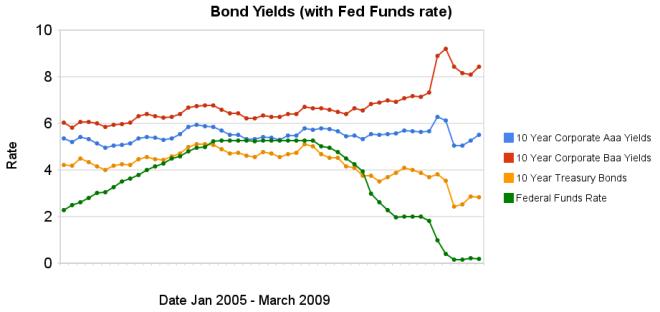

photo of Cesar Augusto SantamarÃa Escoto in his welding workshop, Chinandega, Nicaragua. Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,  Chart showing government debt as a percentage of GDP by Curious Cat Investing Economics Blog,

Chart showing government debt as a percentage of GDP by Curious Cat Investing Economics Blog,