Home prices fall by record 19.1 percent in 1Q

…

New York still is up 73.4% from January 2000, though down 19.7% from its June 2006 peak. The Detroit index is 29% lower than in January 2000. Detroit home prices are back to their mid-1995 levels.

Phoenix, Las Vegas and San Francisco continued to lead year-over-year decliners, with drops over 30%. Minneapolis led month-to-month decliners, as the rate of decline accelerated there. The rates of decline also accelerated in Boston, Detroit, Las Vegas, Miami, New York, Portland, San Diego and Seattle.

Dallas, Denver, Cleveland, Boston and Charlotte managed to avoid double-digit year-over-year declines. Measuring from each market’s peak, Dallas has suffered the least, down 11.1% from its peak in June 2007; while Phoenix is down 53% from its peak in June of 2006. All of the 20 metro areas are in double digit declines from their peaks, with two — Phoenix and Las Vegas — in excess of 50%.

Related: Home Price Declines Exceeding 10% Seen for 20% of Housing Markets (Sep 2007) – Nearly 10% of Mortgages Delinquent or in Foreclosure – Record Home Price Declines (Sep 2008)

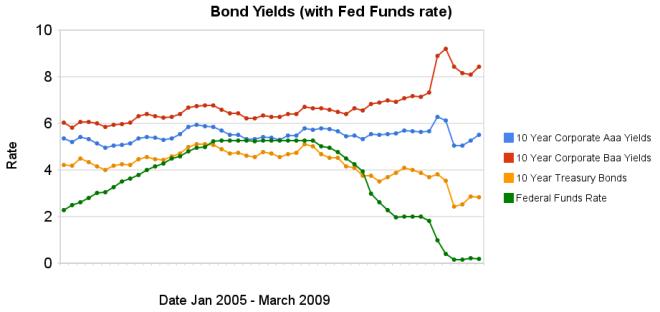

Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields by Curious Cat Investing Economics Blog,