I have posted about the need to save money while you are working numerous times. Here is a good article looking at the large number of people that have failed to do so and are now retiring.

Retiring Boomers Find 401(k) Plans Fall Short

…

Vanguard long advised people to put 9% to 12% of their salaries—including the employer contribution—in their 401(k) plans. The current median amount that people contribute is 9%, counting the employer contribution, Vanguard says.

Recently, Vanguard has begun urging people to contribute 12% to 15%, including the employer contribution, because of the stock market’s weak returns and uncertainty about the future of Social Security and Medicare.

…

Experts estimate Social Security will provide as much as 40% of pre-retirement income, or $35,080 a year for that median family. That leaves $39,465 needed from other sources. Most 401(k) accounts don’t come close to making up that gap.

The median 401(k) plan held $149,400, including plans from previous jobs, according to the Center for Retirement Research. To figure the annual income from that, analysts typically look at what the family would get from a fixed annuity. That $149,400 would generate just $9,073 a year for a couple, according to New York Life Insurance Co., the leading provider of such annuities— less than one-quarter of the $39,465 needed.

Just 8% of households approaching retirement have the $636,673 or more in their 401(k)s that would be needed to generate $39,465 a year.

Knowing exactly what is needed for retirement is difficult. But knowing what is a responsible amount is not. It is certainly no less than 8%, and is likely the 12-15% figure Vanguard recommends. If you start at 10% from the time you join the full time workforce (in your 20’s) then you have some flexibility you can see how thing look when you are 30, maybe 12% is sensible, maybe 15%, maybe 10%. If you fail to save for a decade however, you are likely to need to be at 15%, or higher.

(more…)

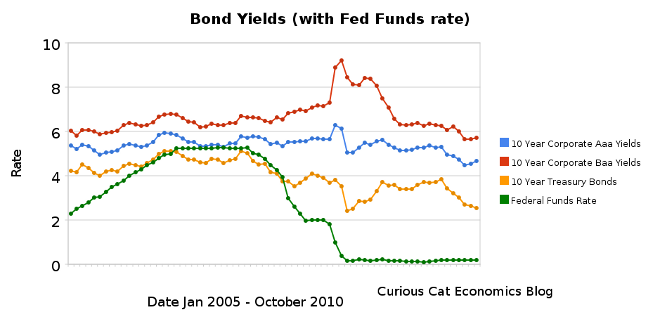

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,