Municipal bonds seem safe. But the incredible long period of irresponsible spending and taking on long term liabilities (pensions, health care costs, infrastructure to maintain) and low taxes and selling off future income streams (to consume today) leaves those bonds with questionable financial backing in many locations. Municipal bond investments should be examined more closely today in light of the problems in the market.

Video shows the State Budgets: The Day of Reckoning by 60 minutes.

Wave of Muni Defaults to Spur Layoffs, Social Unrest: Whitney

Muni experts, including an analyst from Standard & Poor’s, dismissed her predictions, saying the numbers don’t add up.

…

“States clearly have been funding municipal governments—for now up to 40 percent of their total expenditures,” she explained. “As the states become more compromised from a fiscal standpoint, that funding is going to end.”

…

Whitney added that it’s way too soon to see muni bonds as a buying opportunity. But she said that can change quickly.

“When you start to see the first major defaults in this area [the states and cities], when you see more defaults and indiscriminate selling—if you do your research now and figure out who’s protected where and which revenues are protected, there will be great buying opportunities,” Whitney said.

“People are complacent about these defaults. The news about all this isn’t out there yet,” Whitney went on to say. “And only when it is out there, then there will be a buying opportunity [for munis].”

Related: USA State Governments Have $1,000,000,000,000 in Unfunded Retirement Obligations – NY State Raises Pension Age to Save $48 Billion – What the Bailout and Stimulus Are and Are Not – posts on bonds

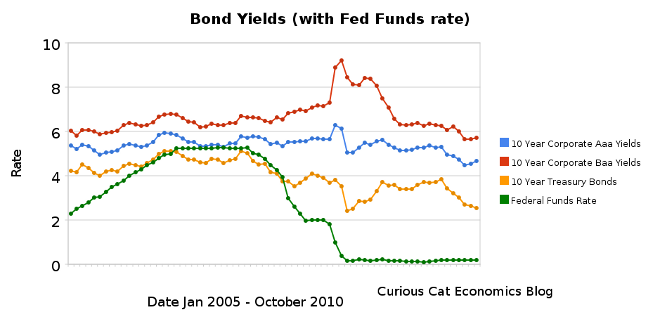

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,