Warren Buffett has published his always excellent annual shareholder letter. It is a pleasure to read them every year, when they are published, and re-read them at other times of the year.

Yearly figures, it should be noted, are neither to be ignored nor viewed as all-important. The pace of the earth’s movement around the sun is not synchronized with the time required for either investment ideas or operating decisions to bear fruit. At GEICO, for example, we enthusiastically spent $900 million last year on advertising to obtain policyholders who deliver us no immediate profits. If we could spend twice that amount productively, we would happily do so though short-term results would be further penalized. Many large investments at our railroad and utility operations are also made with an eye to payoffs well down the road.

…

At Berkshire, managers can focus on running their businesses: They are not subjected to meetings at headquarters nor financing worries nor Wall Street harassment. They simply get a letter from me every two years and call me when they wish.

…

From a standing start in 1985, Ajit has created an insurance business with float of $30 billion and significant underwriting profits, a feat that no CEO of any other insurer has come close to matching. By his accomplishments, he has added a great many billions of dollars to the value of Berkshire.

…

At bottom, a sound insurance operation requires four disciplines… (4) The willingness to walk away if the appropriate premium can’t be obtained. Many insurers pass the first three tests and flunk the fourth. The urgings of Wall Street, pressures from the agency force and brokers, or simply a refusal by a testosterone-driven CEO to accept shrinking volumes has led too many insurers to write business at inadequate prices. “The other guy is doing it so we must as well” spells trouble in any business, but none more so than insurance.

…

a few have very poor returns, a result of some serious mistakes I have made in my job of capital allocation. These errors came about because I misjudged either the competitive strength of the business I was purchasing or the future economics of the industry in which it operated. I try to look out ten or twenty years when making an acquisition, but sometimes my eyesight has been poor.

…

It’s easy to identify many investment managers with great recent records. But past results, though important, do not suffice when prospective performance is being judged. How the record has been achieved is crucial, as is the manager’s understanding of – and sensitivity to – risk (which in no way should be measured by beta, the choice of too many academics). In respect to the risk criterion, we were looking for someone with a hard-to-evaluate skill: the ability to anticipate the effects of economic scenarios not previously observed. Finally, we wanted someone who would regard working for Berkshire as far more than a job.

…

At Berkshire, managers can focus on running their businesses: They are not subjected to meetings at headquarters nor financing worries nor Wall Street harassment. They simply get a letter from me every two years and call me when they wish.

…

From a standing start in 1985, Ajit has created an insurance business with float of $30 billion and significant underwriting profits, a feat that no CEO of any other insurer has come close to matching. By his accomplishments, he has added a great many billions of dollars to the value of Berkshire.

…

At bottom, a sound insurance operation requires four disciplines… (4) The willingness to walk away if the appropriate premium can’t be obtained. Many insurers pass the first three tests and flunk the fourth. The urgings of Wall Street, pressures from the agency force and brokers, or simply a refusal by a testosterone-driven CEO to accept shrinking volumes has led too many insurers to write business at inadequate prices. “The other guy is doing it so we must as well” spells trouble in any business, but none more so than insurance.

…

a few have very poor returns, a result of some serious mistakes I have made in my job of capital allocation. These errors came about because I misjudged either the competitive strength of the business I was purchasing or the future economics of the industry in which it operated. I try to look out ten or twenty years when making an acquisition, but sometimes my eyesight has been poor.

…

It’s easy to identify many investment managers with great recent records. But past results, though important, do not suffice when prospective performance is being judged. How the record has been achieved is crucial, as is the manager’s understanding of – and sensitivity to – risk (which in no way should be measured by beta, the choice of too many academics). In respect to the risk criterion, we were looking for someone with a hard-to-evaluate skill: the ability to anticipate the effects of economic scenarios not previously observed. Finally, we wanted someone who would regard working for Berkshire as far more than a job.

Warren Buffett packs in great lessons all throughout the letter. Read it and take them to heart.

Related: Buffett Calls on Bank CEOs and Boards to be Held Responsible – Warren Buffett’s Q&A With Shareholders 2009 – The Greatest Wall Street Danger of All: You – Warren Buffet Webcast to MBAs – Warren Buffett’s 2007 Letter to Shareholders – Warren Buffett’s Annual Report

(more…)

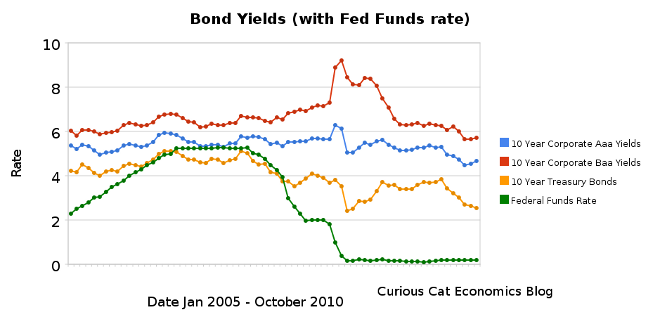

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,

Chart showing corporate and government bond yields from 2005-2010 by Curious Cat Investing Economics Blog,